What Percentage of Income Should Go to Rent in 2026? A Modern Guide for Renters and Property Owners

Introduction: Why Your Rent-to-Income Ratio Matters

Defining the Rent-to-Income Ratio

The rent-to-income ratio is the percentage of your gross monthly income that goes toward monthly rent and utilities. This simple metric empowers both renters and property owners: for renters, it helps in calculating rent you can comfortably afford; for owners, it sets realistic expectations for vetting prospective tenants. Understanding your target rent as a percentage of your income level is the cornerstone of sustainable housing costs and long-term financial goals.

Why This Metric Is Essential for Renters and Landlords

For tenants, exceeding a healthy rent-to-income ratio means less money for debt payments, retirement savings, discretionary spending, and essentials like car insurance or an emergency fund. Meanwhile, property owners use this ratio to evaluate the financial stability of prospective renters, aiming to minimize late rent payments and turnover. Both sides rely on this number to ensure that rent and utilities remain manageable even as the rental market evolves.

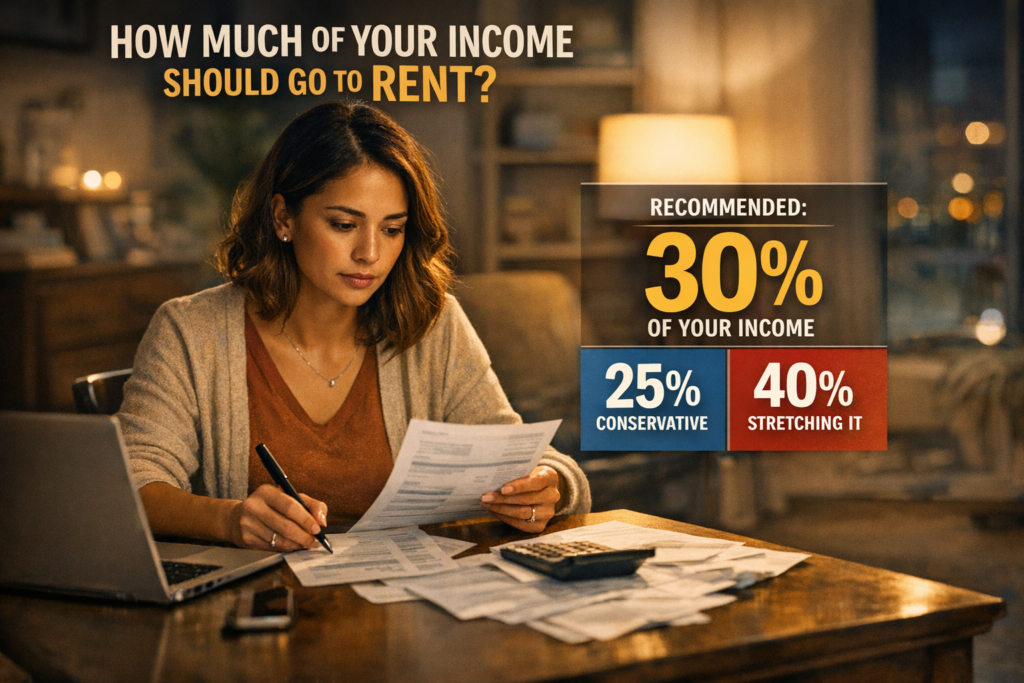

Quick Tips: Most financial experts recommend that your rent payments—including standard utility costs and renter’s insurance—should not exceed 30% of your gross monthly income. This is a starting point; always factor in other expenses unique to your situation.

The Traditional 30% Rule Explained

Origins and Endurance of the 30% Standard

The widely cited “30% rule” began as a federal housing guideline, adopted in the late 20th century to ensure individuals retained enough of their income for essentials and future debt repayment. The logic: keeping total housing costs under 30% of monthly gross income leaves room for minimum debt payments, daily expenses, and building an emergency fund.

The 30% Rule vs. Modern Financial Realities

Yet, in today’s rental market, strict adherence to 30% is increasingly difficult. As one bedroom apartment rents surge—especially in city center locations—median income sometimes fails to keep pace. Should you use gross income or net income (take home pay) for the calculation? Most experts still cite gross monthly income for the exact percentage, as it provides a consistent baseline, but keeping tabs on net income can add crucial context.

For property owners and managers, confirming that a prospective tenant’s monthly rent does not surpass 30% of their gross amount can be a decisive screening step. Still, flexibility remains crucial in today’s evolving market.

Quick Tips: If you’re uncertain about your ideal rent, try a practice calculation: multiply your annual gross income by 0.3 and divide by 12. That figure is your maximum recommended monthly rent, before factoring in taxes, minimum debt payments, and utility costs.

Budgeting Alternatives: The 50/30/20 Rule and Beyond

How the 50/30/20 Rule Compares

The 50/30/20 rule restructures your gross income: 50% should go to essentials like rent, utilities, car insurance, and groceries, 30% to discretionary spending, and 20% to financial goals such as retirement savings or additional debt payments. This rule offers a broader budgeting approach, recognizing that some renters have high student loans or personal loans. It can help you balance housing costs against lifestyle and future-planning priorities.

Zero-Based and Envelope Budgeting Options

Modern renters may find zero-based budgeting or envelope systems more effective, especially when income fluctuates (common among gig workers and small business owners). By budgeting every dollar of your gross income—including exact rent amount, utility costs, and even renter’s insurance—these methods give you maximum control over your monthly rent and other expenses.

Quick Tips: Use a rent calculator to cross-reference your income, housing costs, and debt payments for more accurate, personalized budgeting.

Post-2024 Economic Shifts: Rethinking What’s Realistic

Impact of Inflation and Rising Rent Prices

The years following 2024 brought increased inflation, impacting rental property investments and driving up rent payments across many markets. Even with annual earnings growth in some industries, median income often lags behind rental price hikes, requiring renters to reassess what percentage of income should go to rent while budgeting more for utility costs and renter’s insurance.

Understanding Wage Stagnation and Local Market Pressures

Wage stagnation exacerbates housing cost burdens. In competitive urban centers, renters may be forced to allocate over 35% (or more) of their gross amount to rent and utilities, particularly for high-demand units or those near employment centers. Property owners need to understand these realities when evaluating prospective tenant applications, sometimes adjusting expectations or engaging with local rental assistance resources.

Quick Tips: If your debt payments and rent add up to more than 45% of your gross monthly income, adjust your housing budget or seek assistance to maintain financial health and avoid missed rent payments.

Regional Variations: How Location Impacts Rent Benchmarks

High-Cost vs. Low-Cost Markets

Renting in the city center or coastal regions often means dedicating a larger share of monthly gross income to cover rent, utilities, and even higher security deposits. Meanwhile, low-cost regions or smaller towns allow for more money to be saved for retirement and emergency funds. In all markets, evaluating rent and utilities together—rather than base rent alone—gives a more accurate snapshot of real housing costs.

The Role of Local Policies, Taxes, and Incentives

Regional differences also stem from local tax rates, government incentives, and rent control policies that affect both monthly rent and long-term affordability. Property investors and renters alike must stay informed to make strategic housing and investment choices.

Demographic Drivers: Adapting Rent Strategies by Household Type

Remote Workers and Digital Nomads

Remote workers and digital nomads, often unconstrained by geography, can reduce housing costs by living in more affordable markets—enabling a lower rent-to-income ratio and increased discretionary spending. However, fluctuating income complicates budgeting, requiring careful rent calculations and flexibility with lease terms.

Multi-Generational and House-Sharing Households

Increasingly, multi-generational arrangements or shared rentals allow adults to split the rent amount, stretching annual income and reducing individual housing costs. In these cases, the combined gross monthly incomes set the upper limit for what the household should spend on rent and utilities.

Student Renters and Early-Career Professionals

Students and early-career professionals often lack substantial annual earnings and face higher minimum debt payments, especially on student loans. For this demographic, paying rent below 30% of gross income—often by sharing a one bedroom apartment or opting for less expensive neighborhoods—is crucial to avoid overwhelming debt repayment burdens.

Quick Tips: Consider your debt-to-income ratio as well as rent-to-income when evaluating affordability. If debt repayment and rent stretch your budget, explore options for house sharing or less central locations.

2026 Outlook: Updated Recommendations for Optimal Rent Allocation

Scenario-Based Guidance: Tight Markets vs. Affordable Regions

Looking ahead to 2026, the traditional 30% rule remains a sound guide, but it’s vital to adapt your rent strategy based on housing supply, rental market trends, and your personal financial landscape. In high-demand markets, spending up to 35% of monthly income may be justifiable—if other expenses and discretionary spending remain controlled. In more affordable regions, stick closer to the 25–28% range, allowing for additional savings and investments.

Personalized Assessments: Tools and Calculators

Renters and owners benefit from precise, data-backed planning tools. KT Rents offers a rent calculator to help you determine your ideal rent amount based on gross income, net income, debt payments, and local market data. For more comprehensive analysis, our rent vs buy calculator can help compare long-term housing scenarios.

Navigating Trade-Offs: What Happens If You Stretch Beyond the 30% Mark?

Short-Term and Long-Term Implications

Paying rent that exceeds 30% of gross monthly income can lead to trade-offs: delayed retirement savings, increased reliance on personal loans, reduced emergency funds, and greater exposure to housing instability if income drops. Prospective renters in these situations should weigh the risks of high rent payments against lifestyle priorities and job security.

Proactive Strategies to Stay Financially Healthy

To avoid financial stress, set strict budgets for utility costs, minimize discretionary spending, and compare total housing costs (rent and utilities) to your take home pay. If current housing costs are unsustainable, consider negotiating your lease, seeking roommate arrangements, or leveraging rental assistance.

Quick Tips: If you regularly struggle to pay last month’s rent or security deposit, it might be time to revisit your housing budget. Responsible adaptive strategies could include subletting, moving to a smaller unit, or seeking a more flexible lease arrangement.

Rental Assistance and Resources in 2026

New Government Programs and Grants

By 2026, expanded federal and state rental assistance programs support tenants whose rent payments exceed 30% of gross amount or who face economic hardship. These include direct payment grants, utility subsidies, and temporary eviction prevention funds.

Private and Community Support Options

Private charities and local community organizations offer additional debt payments relief, moving cost assistance, and housing navigation services for both renters and property owners. These resources bridge gaps when gross income limits access to safe, quality rentals in the desired rental market.

How KT Rents Connects Tenants and Owners to Local Services

At KT Rents, we actively connect clients to vetted support services and updated information on grants. We guide both renters and landlords through available channels to ensure successful, stable tenancies despite income level fluctuations.

How KT Rents Helps You Optimize Your Rent-to-Income Ratio

Our Approach to Transparent Rent Setting

We pride ourselves on clear, market-based rental pricing and honest lease agreements. By leveraging current rental market data and analyzing your gross monthly income and other expenses, we set fair rent amounts that support long-term tenant stability and asset value.

Value-Driven Leasing and Tenant Placement

Our candidate screening incorporates income verification, minimum debt payments, and rental history. As expert property managers, we focus on matching renters to units where they can comfortably afford all housing costs. Owners can trust KT Rents for efficient, data-driven vacancy management and reliable rent payments.

Internal Link: Learn more about our tenant screening services

For more on optimizing your rent-to-income ratio and securing dependable renters, explore our property management and tenant screening guidance here.

Conclusion: Planning Your Housing Budget for Success in 2026

Key Takeaways for Renters and Property Owners

There is no single “exact percentage” of income that fits every scenario. Still, aiming to keep rent and utilities below 30% of your gross monthly income remains a strong benchmark for most households. Regular review of your housing costs, debt repayment, discretionary spending, and use of reliable online calculators will ensure your budget supports your goals, not just now, but for years to come.

Internal Link: Explore KT Rents’ Insights Hub for More Resources

Continue your research and access actionable rental advice at our Insights and Resources blog. For homebuyers, see how your rent-to-income ratio compares to purchasing scenarios on our Renting vs. Buying Guide.